All Categories

Featured

Table of Contents

If you take a distribution versus your account prior to the age of 59, you'll also have to pay a 10% penalty. The IRS has imposed the MEC regulation as a method to protect against people from skirting tax commitments. Limitless financial only functions if the cash value of your life insurance coverage policy continues to be tax-deferred, so make sure you do not turn your policy right into an MEC.

Once a cash worth insurance coverage account classifies as an MEC, there's no means to reverse it back to tax-deferred condition. Limitless banking is a practical principle that offers a selection of benefits.

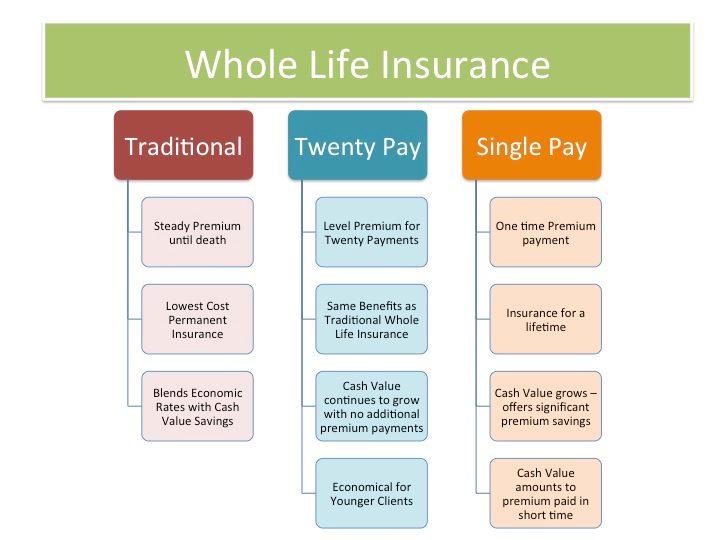

You can enjoy the benefits of boundless banking with a variable universal life insurance policy plan or an indexed universal life insurance coverage policy. However considering that these kinds of policies tie to the securities market, these are not non-correlated possessions. For your policy's money value to be a non-correlated asset, you will certainly need either entire life insurance policy or global life insurance policy.

Before picking a policy, discover if your life insurance coverage business is a mutual firm or not, as only mutual companies pay dividends. The next time you require a large amount of money to make a down settlement on a home, pay for college tuition for your children, or fund a brand-new financial investment You will not have to dip into your financial savings account or search for loan providers with low-interest prices.

How does Infinite Banking For Financial Freedom compare to traditional investment strategies?

By taking a funding from you as opposed to a typical loan provider, the customer can save hundreds of bucks in interest over the life of the funding. (Just be sure to charge them the very same interest rate that you have to repay to yourself. Or else, you'll take a financial hit).

It's simply another way to defer paying taxes on a section of your revenue and develop an additional safeguard for on your own and your family. But there are some downsides to this financial method. Since of the MEC legislation, you can not overfund your insurance plan excessive or as well swiftly. It can take years, otherwise decades, to build a high money worth in your life insurance policy plan.

A life insurance coverage policy connections to your health and life span. Depending on your medical background and pre-existing conditions, you may not qualify for an irreversible life insurance coverage plan at all. With unlimited financial, you can become your own banker, obtain from on your own, and add money worth to a long-term life insurance coverage plan that grows tax-free.

When you first become aware of the Infinite Banking Principle (IBC), your very first reaction may be: This sounds too excellent to be real. Possibly you're cynical and believe Infinite Banking is a scam or system. We desire to establish the record straight! The problem with the Infinite Banking Concept is not the idea however those persons supplying an adverse review of Infinite Financial as a concept.

As IBC Authorized Practitioners with the Nelson Nash Institute, we assumed we would address some of the leading inquiries people search for online when discovering and comprehending whatever to do with the Infinite Financial Principle. What is Infinite Banking? Infinite Financial was developed by Nelson Nash in 2000 and totally clarified with the magazine of his publication Becoming Your Own Banker: Open the Infinite Banking Idea.

What do I need to get started with Infinite Banking Retirement Strategy?

You think you are coming out monetarily ahead due to the fact that you pay no rate of interest, but you are not. When you conserve cash for something, it normally suggests giving up something else and reducing on your lifestyle in other locations. You can repeat this process, but you are simply "reducing your method to wealth." Are you satisfied living with such a reductionist or deficiency frame of mind? With saving and paying money, you may not pay rate of interest, however you are using your money as soon as; when you invest it, it's gone forever, and you offer up on the chance to gain life time compound rate of interest on that money.

Billionaires such as Walt Disney, the Rockefeller family and Jim Pattison have leveraged the residential or commercial properties of whole life insurance policy that dates back 174 years. Also financial institutions make use of entire life insurance for the exact same objectives. It is called Bank-Owned-Life-Insurance (BOLI). The Canada Profits Agency (CRA) even identifies the value of getting involved whole life insurance policy as a special possession course made use of to create long-term equity securely and naturally and provide tax obligation advantages outside the range of standard investments.

What happens if I stop using Infinite Banking Vs Traditional Banking?

It enables you to produce wealth by meeting the banking feature in your own life and the capability to self-finance major way of life purchases and costs without interrupting the compound interest. Among the most convenient means to think of an IBC-type getting involved whole life insurance coverage plan is it approaches paying a mortgage on a home.

Gradually, this would certainly create a "consistent compounding" effect. You understand! When you borrow from your getting involved entire life insurance policy plan, the cash worth remains to expand nonstop as if you never borrowed from it to begin with. This is because you are utilizing the money worth and survivor benefit as collateral for a loan from the life insurance policy company or as security from a third-party lender (referred to as collateral lending).

That's why it's critical to deal with a Licensed Life Insurance policy Broker licensed in Infinite Banking who structures your getting involved entire life insurance coverage policy properly so you can prevent unfavorable tax obligation implications. Infinite Banking as an economic approach is except everyone. Below are a few of the pros and cons of Infinite Banking you ought to seriously consider in choosing whether to progress.

Our favored insurance coverage provider, Equitable Life of Canada, a common life insurance policy firm, focuses on participating whole life insurance policy plans specific to Infinite Financial. Likewise, in a common life insurance coverage business, insurance holders are considered firm co-owners and get a share of the divisible surplus generated each year via rewards. We have a range of providers to select from, such as Canada Life, Manulife and Sunlight Lifedepending on the demands of our customers.

What makes Private Banking Strategies different from other wealth strategies?

Please additionally download our 5 Top Concerns to Ask A Limitless Banking Representative Prior To You Employ Them. To find out more regarding Infinite Financial see: Disclaimer: The material offered in this e-newsletter is for informative and/or academic functions only. The information, point of views and/or sights revealed in this newsletter are those of the writers and not necessarily those of the distributor.

{kind=link}

Latest Posts

R Nelson Nash Infinite Banking Concept

Infinite Banking Concept Example

How To Be Your Own Bank In Crypto